Wealth Taxes in Europe

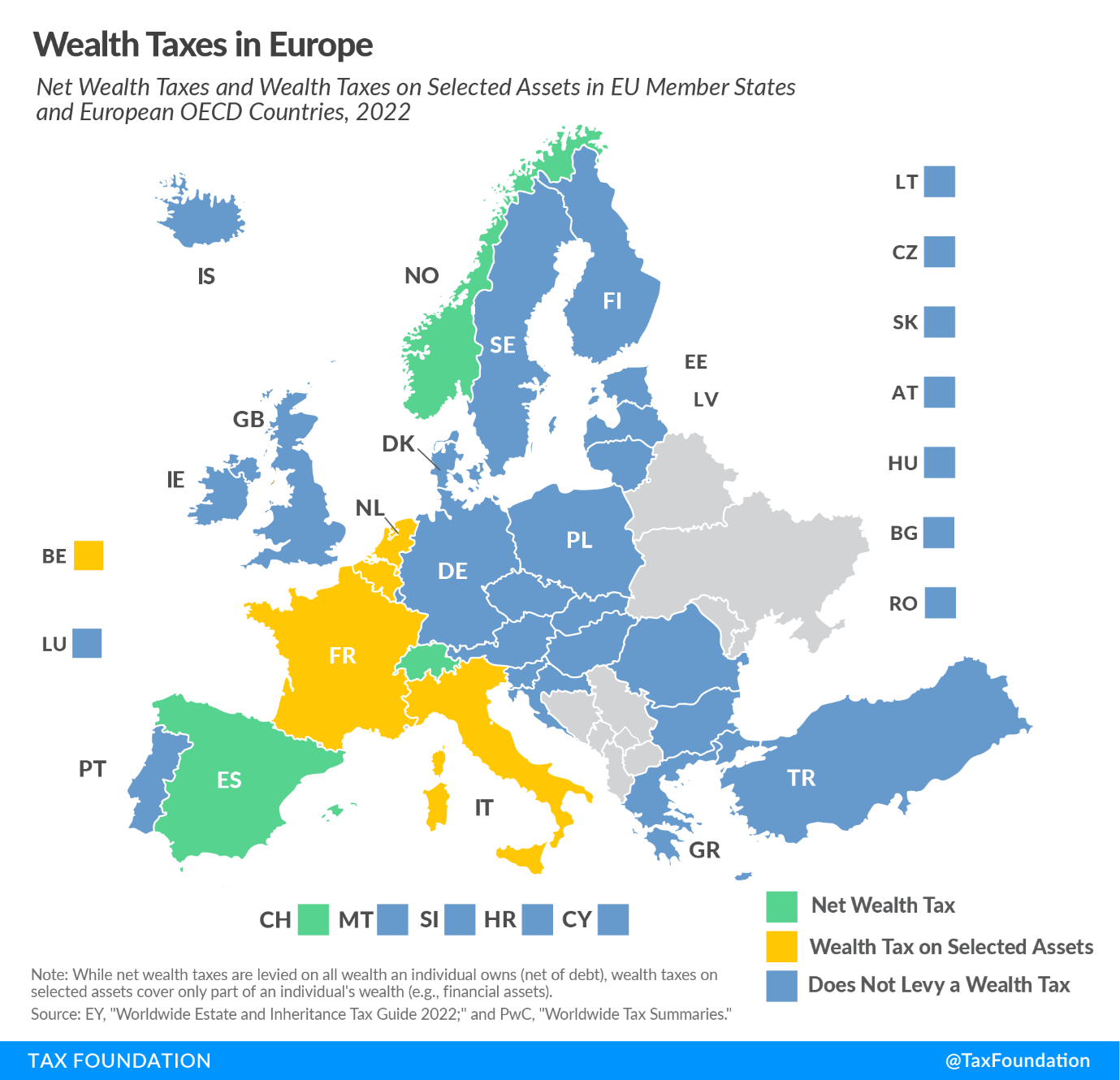

Wealth taxes are recurrent taxes on an individual’s wealth, usually they are net wealth taxes, net of debt. A net wealth tax is similar to a real property tax, but it covers all wealth an individual owns. Only three European countries levy a net wealth tax—Norway, Spain, and Switzerland. France and Italy levy wealth taxes on selected assets by the taxpayer, and so do Belgium and the Netherlands.

Net Wealth Taxes

Norway has had a net wealth tax since 1892. Norway levies a net wealth tax of 0.95% on individuals’ wealth stocks exceeding NOK 1.7 million (€145,000). Additionally, for net wealth exceeding NOK 20 million (€1,710,000), the tax rate is 1.1 percent.

Spain’s net wealth tax is a progressive tax ranging from 0.2 percent to 3.75 percent on wealth stocks above €700,000. However, the autonomous regions have reduced the rates (Madrid and Andalusia offer a 100% relief). Spanish residents are subject to the tax on their worldwide estate while non-residents pay the tax only on assets located in Spain.

Additionally, the Spanish central government introduced a “solidarity wealth tax” ranging from 1.7 percent to 3.5 percent on individuals with net assets exceeding €3 million for 2022 and 2023. Under this new scheme, the central government collects any additional revenue from the solidarity tax once the regional wealth tax collection is deducted. This wealth tax will affect taxpayers in who live in a region that approved a higher tax exemption threshold or lower tax rates than the national rates.

Switzerland implemented its wealth tax in 1840. Switzerland levies its net wealth tax at the cantonal level and covers worldwide assets (except real estate and permanent establishments located abroad). The tax rates and allowances vary significantly from one canton to another.

Wealth Taxes on Selected Assets

France introduced a net wealth tax in 1981 but replaced it in 2018 with a real estate wealth tax. French residents are liable to the tax when their net worldwide real estate is worth €1.3 million or more. Non-residents are only liable to the wealth tax if their net real estate located in France are valued at €1.3 million or more. Depending on the net value of the real estate, the tax rate ranges from 0.5 to 1.5%.

Italy taxes financial assets held by individual resident taxpayers outside Italy without Italian intermediaries ; the tax is 0.2%. Additionally, real estate held by Italian tax residents outside Italy are are taxed at 0.76%.

After a failed attempt to tax holders of securities accounts, Belgium introduced an annual tax on securities accounts of 0.15% on securities accounts with an average value of €1 million.

In the Netherlands, the value of net wealth (excluding primary residence and substantial interests in companies) is included in the income tax, with effective tax rates ranging from 0.56 percent to 1.78 percent with a deemed income in “box 3 income”. In 2021, the Dutch Supreme Court ruled that this system violates European Law regarding non-discrimination and property rights. In 2022, an alternative system was proposed where each asset category—savings, debts, and others—would have its own deemed return. 2022 was a transition year where taxpayers had to choose between the the old system and the new proposal to be taxed.

While wealth taxes collect little revenue, an OECD report argues that wealth taxes can disincentivize entrepreneurship, harming innovation and long-term growth. In practice, the recent wealth tax developments have pushed Spain’s regional governments to appeal the “solidarity wealth tax” to the Constitutional Court. Additionally, Norway approved a higher exit tax as billionaires are leaving the country.